Measuring whether strategic objectives and desired benefits from transformation programs are being realized is important for organizations. By actively directing their efforts toward realizing benefits, organizations can maintain focus, thus enabling them to be more successful in realizing their strategy. In addition, an active focus on benefits ensures more and better integrated management of such transformations, which presents the opportunity for better decision-making.

Introduction

When organizations undergo transformations, the aim is to better realize the organization’s strategic plan. Such transformations involve, for example, changes that equip the organization for shifts in the market, changes that reduce costs, and changes that introduce new (information) technology. Almost seventy percent of all transformations are regarded as somewhat or largely successful, while less than ten percent are seen as wholly successful ([McKi06]). These may be catchy statistics, but imagine what it might mean to your organization if a transformation is better than “somewhat” successful, and is largely or even wholly successful. What would be the impact of this on your colleagues, clients and shareholders?

It would undoubtedly have a major impact. The question is, then, how can we realize improved benefits, and consolidate them for the long term? Several success factors play a role in this process. This article deals with one of the success factors, namely, developing a focus on realizing benefits from transformations.

Benefits are the financial and non-financial advantages that an organization wishes to achieve — such as more turnover or customer satisfaction, for instance. Research has shown that the degree to which benefits are realized in change projects can be improved by structuring the project to focus on benefits ([Ward06]). On the one hand, this can be done by bringing the ultimate goal into focus and effectively communicating about the necessary change. On the other hand, it can be done by measuring the interim progress made during the transformation, where adjustments can be made and expectations can be managed. This ensures that everyone is clear about their role, and what is expected in achieving the stated goal.

This article deals, first of all, with the issue of why, during transformations, organizations should pay attention to benefits. At such a time there are a thousand other things to be done, which may seem much more important or urgent. The article goes on to cover how benefits management should be designed, and identifies some discrete steps. Pursuing benefits ensures that all eyes are focused on the real goal.

Why apply benefits management during transformations?

The large scale of transformations often demands a lot of an organization. Accordingly, as research has shown, it is not surprising that there are many ways of improving the success of transformations. There may be room for improvement in translating the strategy, measuring the impact, and identifying accountability ([HBR10]). Benefits management can make a significant contribution to reinforcing these areas of possible improvement by making the benefits measurable. That means identifying how the implemented changes contribute to the realization of strategic aims. This subsequently provides a good basis for identifying the role of success factors such as communication, the definition of clear milestones, KPIs and structures ([McKi10]).

The most important contributions to benefits management are:

- it connects strategy and execution

- it makes change measurable and manageable

- it leads to better decision-making.

In conjunction with costs, progress and risks, which are often already measured, measuring benefits offers a good basis for improving the chances that the transformation will be successful.

Benefits management connects strategy and execution

The first important contribution of benefits management is that it connects the strategy and execution. It does this by setting out the way the strategy is to be achieved. Subsequently, during the transformation, it provides interim evaluation. This feedback on the progress of the project allows adjustments to be made where necessary. Feedback and adjustments apply to both the project activities and the line activities. In this way, any changes in the line (such as behavior or working method) that are necessary to achieve the intended goals are made transparent. Having a new customer relationship management system, for example, provides no added value in itself. It is only when the organization adapts its behavior to this new relationship and actually uses the system to realize extra sales (by means of cross-selling, for example), that the benefits begin to accumulate. Often, the project activities are clear, but there is less insight into the change activities that are needed in the line organization in order to realize the benefits.

During large-scale transformations insight into the associated change activities is particularly important, due to their strategic significance. In this context, it must be clear what all programs, projects and business units ought to contribute to ensure that the transformation is a success. This clarity subsequently provides the basis for the necessary dialog on the aim, approach and pace of the transformation. Clarity and transparency helps give direction to the transformation and breach the status quo ([Mile10]). After all, transformations often lead to major alterations in structure, behavior and relationships. Acting on the basis of emotions or allowing political preferences to prevail can derail a transformation at an early stage.

Benefits management makes changes measurable and manageable

The second contribution of benefits management is that it makes change measurable. And, in the spirit of management guru Peter Drucker, what you measure is what you get. Making change measurable in terms of specific KPIs conveys a clear message about the desired behavior. The KPIs against which leaders are held to account are aligned with the intended aims of the transformation, and conflicting KPIs are analyzed. Consolidating this desired behavior with performance measurement (the Balanced Scorecard, for example) helps in achieving enduring results.

In addition, making change measurable ensures that adjustments can be executed in good time. After all, activities or projects do not automatically lead to results ([Skin04]). A good example of this is that the purchase of a rowing machine (action) does not automatically lead to loss of weight (desired result). To gain the desired result, an active policy must be followed with regard to performance (such as frequency, distance covered and speed) and health (heart rate and calorie consumption) (after [Hunt09] and [Kell11]).

Benefits management leads to better decision-making

The third and final reason for applying benefits management in transformations is that it leads to better decision-making. This improvement is made possible by increased clarity and measurability, and by establishing responsibility for realizing certain changes and the corresponding benefits. Research has shown that exactly these aspects – information and clarity about who decides what – are major factors in turning strategy into success ([Neil08]).

Good decision-making is also important in view of the fact that, during these transformations, organizations often have to cope with changing circumstances and developing insight. What if one of the competitors suddenly taps into a new market, earlier than expected? Is it still realistic to attempt to capture the previously estimated market share? Those prior estimates may figure into the current strategy, and may need to be revised. Of course, such issues concerning the changing environment play a role in all changes and projects. However, in the case of transformations, this effect is magnified by factors such as duration, strategic character and size, which often extends over several business functions and several countries. Making information measurable and clarifying who decides what leads to qualitatively better decision-making, and also ensures that the decisions made are in line with an explicit strategic direction. Monitoring the benefits also enables the organization to make decisions earlier: it becomes immediately clear if, for example, results in subprojects are falling short, or deviate from the intended strategic direction.

In this way, focusing on benefits management during transformations provides a basis by which other success factors can be more easily measured. This reinforces their positive effect on the success of transformations.

In summary, this section makes it obvious why benefits management is extra important in the case of transformations. A transformation is a very dynamic process. As a consequence, there must be continual reflection on the developing situation and on changing expectations for the future. Applying benefits management helps organizations keep the overarching goal of the transformation relevant and realistic.

The following section deals with the approach to benefits management in transformations.

Approach

Now that the possibilities of benefits management have been made clear, the question is how to implement it. Just like every evaluation process, benefits management consists of two main parts: foresight and hindsight. At the start of the transformation, an organization determines the intended benefits. Organizations should then look back periodically to evaluate the extent to which those benefits have been realized. They should also look to the future to estimate whether the anticipated benefits are still realistic, or whether expectations must be adjusted. New benefits may even appear to be possible. Within these cycles of evaluation, there is a continual focus on pursuing appropriate goals, while readjusting as necessary. Benefits management is certainly no one-off exercise.

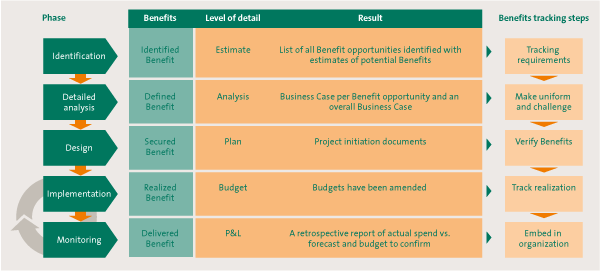

The following subsections describe the nature of the approach. First of all, we deal with identifying the benefits and then developing these benefits into concrete plans. Then we examine the approach to realizing benefits and the management of this approach. The activities of looking forward and looking backward are covered. This approach is schematically represented in Figure 1. In our experience, it is particularly important to pay additional attention to the intermediate steps in this model (detailed analysis, design and implementation). Attention to the benefits and the approach to realizing them tends to wane in these intermediate stages.

Figure 1. Approach to the layout of benefits management.

Identification: from strategic aims to activities

It is necessary to identify the relevant benefits and to create a coherent picture of how they will be realized. In short, identifying the benefits involves only two questions: “What does this give us?” and “Why do we want it?” Repeatedly applying these criteria ensures that the actual benefits are identified, rather than merely the behavioral activities. As a result, a sharp image is created of what concrete advantages the change will bring. In this context, recall the previously mentioned example of a CRM system in which people had to adapt their behavior or working style to achieve the benefit of generating extra sales, using methods such as cross-selling, for example.

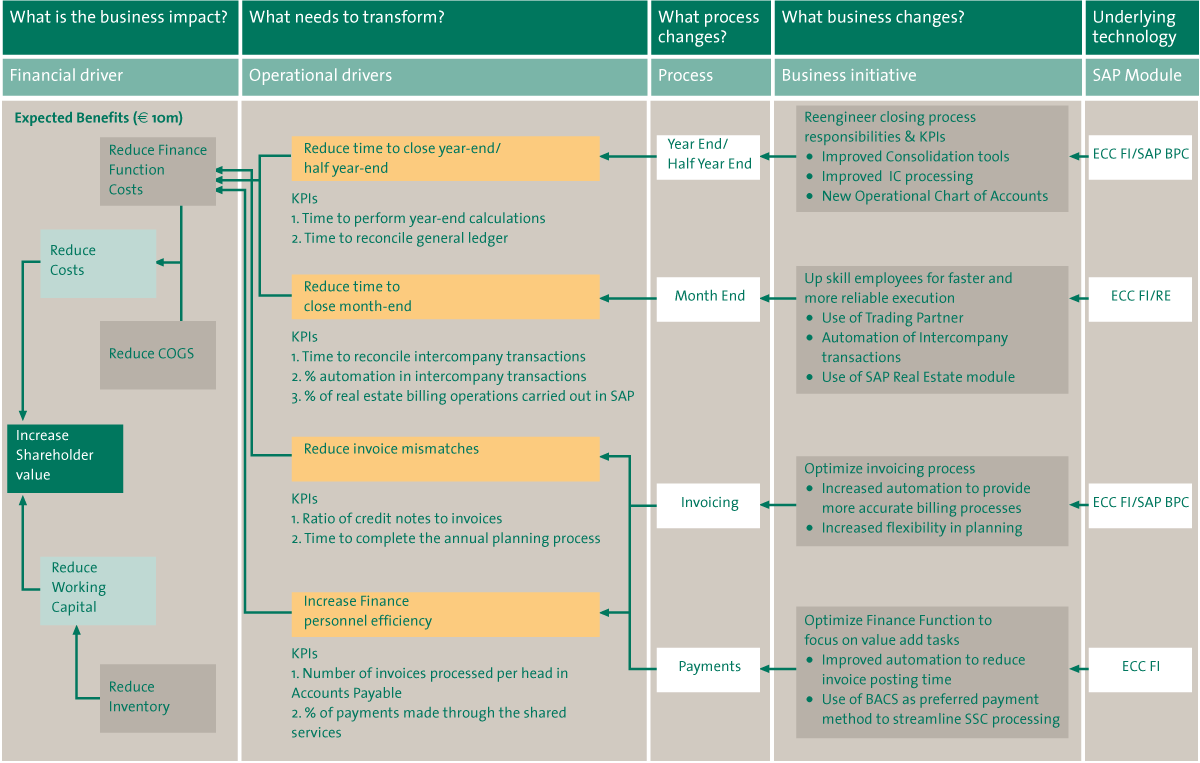

The second step is to establish the relationship between the activities and the goal of the transformation. In other words, how can we reach our goals? Ultimately, all activities must support the transformation in one way or another. To determine whether or not this is truly the case, a coherent image can be developed in a dependency diagram ([Ward06]). This diagram brings clarity to the relationship between change and strategy, so that strategy and execution are linked together.

A completed diagram is shown in Figure 2. It is completed from left to right. This example shows how each of the modules to be implemented contributes to attaining the goal. The transformation, as well as the strategy behind its execution, is the point of departure. At the end of the day, all efforts are geared to enabling the transformation to succeed. The ultimate goal depends upon realizing benefits throughout the organization. To realize these benefits, certain changes have to take place in the organization. In turn, these changes depend upon certain preconditions.

Figure 2. The benefits realization diagram displays the relationship between activities and strategy. [Click on the image for a larger image]

Take, for example, a production company that plans to implement a strategy aimed at achieving cost leadership. For this strategy to succeed, transportation costs must be reduced, which would generate a benefit to the organization. However, this reduction will not happen of its own accord; the business must integrate the logistical flows between factories. Changes in plans and itineraries are inevitable. Adjustments to the planning information system appear to be necessary, so this is an essential precondition.

When the diagram has been formulated, it can also be read from left to right. In that case, the diagram communicates the story of which activities lead to which benefits. Ask yourself if the way in which each activity contributes to the goal is perfectly clear. Are all the steps necessary? Is it perhaps possible to gain extra advantages from activities that are going to be undertaken anyway? And does the diagram show all the activities that are essential for realizing the aims of the transformation?

This benefits realization diagram is a powerful instrument because it shows the activities, intermediate advantages and the strategic aims of a transformation, all in a single image. The diagram can subsequently be used in internal communications by the organization, and clearly shows how the activities of individuals contribute to the higher goal.

Detailed analysis: elaboration of the benefits plans

After obtaining a complete picture of the expected benefits, the next step is to work out the benefits plan with regard to each benefit. The aim of this benefits plan is to acquire detailed insight into the activities required to realize the benefits and to make the change measurable, which makes managing the project easier. These plans include a number of aspects that are important for achieving the benefits. These aspects are discussed in this subsection.

First, give a concrete description of the benefit. It may be set out in one or two words in the diagram, but then needs to be defined more closely. For example, improvement of “customer satisfaction” might be directed toward only a few customer segments and in particular their purchasing departments, but applies to all regions.

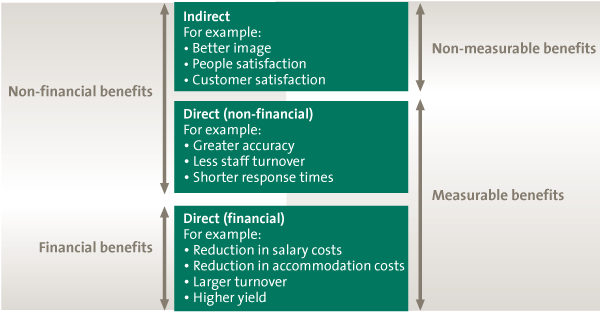

Next, determine how to measure the benefit. There are various sorts of benefits that are measurable to a greater or lesser extent (see Figure 3). Customer satisfaction might be harder to measure than a decrease in salary costs, for example. Therefore it is important to choose the proper indicators to make the benefit measurable. These may include customer-satisfaction surveys, waiting times at service counters, or even the consumer response in tweets with regard to the organization and its products.

Figure 3. The measurability of benefits ([OGC03]).

Then consider how the benefit is intended to develop: what is its present value, its potential value, and how can you reach that potential? Formulating benefits in relative terms anticipates changing circumstances. For instance, identify the goal of reducing the cost price by ten percent, which, with current volumes and cost-price levels, would result in realizing a benefit of X euros. Formulating the goal as a percentage can be better measured and subsequently more effectively adjusted than a fixed goal, particularly in cases of large volume or raw-material price developments. You should also determine the period in which the benefit is to be realized and whether or not this development will be linear or will gradually evolve.

In addition, the benefits plan should state who exactly is responsible for realizing the benefit. In general, this will be a manager who can implement the behavioral, workforce-related changes in the department where the benefits are expected. Accordingly, it is often advisable to involve this person in formulating the benefits plan right from the outset. This contributes to better decision-making. If no one accepts ownership of a benefit, this will significantly reduce the chances of realizing it. Therefore, the benefit should be scrapped completely from the list.

After the benefits plans have been formulated and discussed with the relevant managers, it is advisable to jointly run through the entire benefits realization diagram once again. This time be especially critical. Perhaps the elaboration of the benefits plan will have led to new insights. It may also be good to examine a number of scenarios. Subsequently, the plans should function in harmony in moving toward realizing benefits. This is further covered in the section on “Implementation and monitoring.”

Design: configuring the approach

In addition to determining the substance of the anticipated benefits, organizations must also consider their approach to these benefits. This approach is often set out at the planning stage while the nature of the benefits is being shaped, because this approach requires a determination of who is going to work out the benefits plan and how. After all, the nature of the transformation may vary. One can choose a top-down approach that offers clarity (in a transformation involving cost savings, for example). Alternatively, a bottom-up approach that ensures more collaboration and support for the change at this early stage could be better in a transformation toward a more innovative or customer-oriented organization, for example.

Determining the approach to benefits realization affects the structure that is needed to realize the benefits. This depends on numerous factors. Cost saving or a merger, for example, requires a different emphasis within the process. And whereas one organization may profit from a strict, formal process, the other one may wish to avoid this at all cost. Besides differences based on the nature of the organization and the transformation, there can also be differences between departments (such as sales and finance) or regions. These might all lead to different approaches in realizing benefits.

The way in which responsibility for realizing the benefits is embedded in the organization must also be established. For instance, during organizational change, it is a matter of debate whether the responsibility for benefits realization should be immediately allocated to the future process manager, right at the outset. An alternative would be allocating it first to the functional managers who are still responsible for subprocesses. Establishing responsibility ensures that it is clear who has the mandate to take which decisions, so that decisions do not remain “in limbo” between the old and the new world.

In addition, determining the approach involves deciding how the benefits will be monitored, as well as how they will be pursued. In this context, the key issue is how closely do you wish to oversee the process. Do you wish to monitor all the benefits in detail, or will you choose several indicators that give a good picture of the degree to which the benefits are realized? This process is related to current performance measurement: the extent to which something like the Balanced Score Card can be applied in such a framework. If possible, it is often advisable to align reporting frequency with performance measurement. In turn, this influences the specification of who is engaged in monitoring and how and when reports are presented. At the same time, this alignment determines the feedback moments and when adjustments, if necessary, must take place.

These activities always cost time and effort. At the same time, transforming an organization creates demands on available resources from all sectors. To promote the success of benefits management, efforts must be consolidated in the planning schedules, in the estimates of the transformation costs, and in line management.

Benefits management is ultimately about realizing the aims of the transformation. In that sense, benefits management more or less involves creating a mindset oriented toward realizing value for the business. In many organizations, project managers will already be engaged in ensuring that all activities contribute to the successful conclusion of a project. By placing emphasis on the benefits, an organization ensures that the stakeholders jointly investigate ways to gain benefits from the project. Therefore, it is important to make sure that this mindset becomes rooted in the organization. People must be informed of what is expected of them and how they can meet these expectations. Keep in mind that benefits management is a means rather than an end, and that the approach must harmonize with (and not obscure) the real goal. An interesting example of this was the World Football Championship in which (at least from a European point of view) it was hardly possible to enjoy a game on American television because extensive statistics were shown on screen with great frequency.

Implementation and monitoring: management geared to the realization of benefits

Transformations are exceptionally dynamic processes. That being the case, it is naïve to expect that all benefits can be realized precisely according to the initial plans. That’s why organizations need to determine how they will approach managing the pursuit of benefits, as discussed in the previous step. During the transformation, this management can be divided into two components: monitoring the realization of benefits, and periodically adjusting the benefits plans.

In the monitoring, the benefits realized are compared to the expectations in the benefits plans. The person responsible for realizing the benefit (the designated benefit owner) is asked to give an explanation of any differences. If the current realization is lagging behind the expectations, it is important to investigate why. Not complying with an indicator may not seem like a big deal, but the underlying cause may have significant consequences for the transformation. One should also consider whether the plans for the future are truly realistic, or is adjustment necessary? And what should be adjusted, the activities or the indicator?

This scrutiny not only applies to failures to meet targets. The benefits that do meet targets must also be reconsidered. A small alteration in the surroundings, for example, may have a major effect on whether or not there is a real benefit achieved. One should investigate whether the benefits are appropriate in view of the aim of the transformation, because new insights may arise here, too. Moreover, real-life practice may show that the aims can be adjusted upward or that new and greater benefits can be achieved. It would be a lost opportunity if this option were not taken.

Monitoring requires openness and the sharing of information and insight. Especially when failures to meet targets have been identified, there is a real risk that this monitoring may be confused with singling out staff members for performance issues. When this occurs, the quality of monitoring declines because staff members may attempt to conceal future problems. Therefore one should be careful to ensure that the focus remains on the transformation and on a successful conclusion.

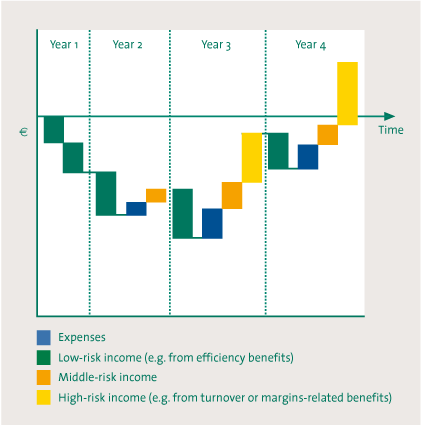

Figure 4 shows how to monitor the cashflow of a project: it shows income from financial benefits in relation to expenditure. Here, the costs of the transformation are set against the expected income from (financial) benefits. The income has been subdivided according to the risk that the benefits will not be achieved. Benefits that are difficult to realize and/or are uncertain (such as increase in turnover) can be classified as “high risk.” An example of a low-risk benefit would be efficiency improvement in a production department that already has a good track record in that field. The figure provides good insight into the way in which the general feasibility of financial benefits changes over the course of time. Such change may be a consequence of delayed activities or a shifting market situation, for example. It also shows the effect of this upon the cashflow for the transformation.

Figure 4. Example of the cashflow of a project, with costs and income from the benefits.

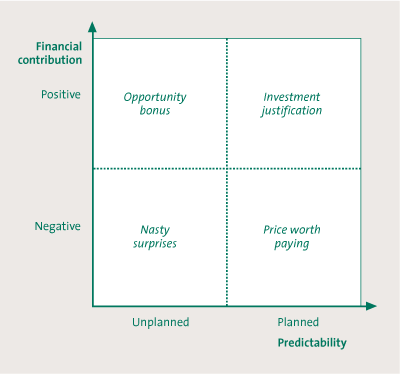

In addition to monitoring, it is also advisable to recalibrate the benefits plans periodically. This could be done annually, for instance, preferably in combination with the recalibration of the project plans for the transformation. This is important because, after about a year, complacency often arises, as things are running smoothly, almost automatically ([Mile10]). This recalibration provides the chance to capitalize on benefits achieved and the progress that has been observed during monitoring, as well as to recalibrate the plan to accommodate factors such as the progress of the transformation and market developments, for instance. In terms of broad-based support, it is advisable to involve benefit owners and to investigate, jointly with them, if more benefits may be achievable and if the transformation could be accelerated. In this process, it is important not only to focus on the planned (positive) benefits but also to identify unplanned benefits, and to include these in the plans in order to manage them better (see also Figure 5).

Figure 5. Benefits management matrix ([Ward06]).

As this article has clearly shown, benefits management is not a separate discipline but rather a perspective that ought to be utilized in the planning and management of a transformation. In our view, this perspective contributes to a more complete picture in the management of transformations, so that they can be realized more successfully. The case presented below demonstrates how the approach outlined can lead to success in real-life practice.

PostNL as an example of benefits management

With its postal activities, PostNL has positioned itself in the Dutch market as a postal service company with the best “value for money,” comparable to Albert Heijn, KPN and KLM in other markets. Due to the complete liberalization of the postal market, and viable alternatives as the result of digitization, the price point has become enormously important. This is especially so for postal services with less competitive service margins. In combination with a declining postal market, this has led to pressure on profit margins.

To preserve profitability, the organization was compelled to reduce and adapt the costs of its infrastructure. PostNL introduced a new business model dividing the distribution week in peak and off-peak days. Customers are offered a specified-day product on peak days, at a reduced rate. The corresponding centralization of the core activities of collecting, sorting, preparing and delivering ensures that PostNL is currently realizing one of the largest transformations ever seen in the Netherlands ([Post11], [Hest09]).

This new business model with its peak and off-peak days means increasing labor flexibility (fewer full-time staff), and increasing task specialization (fewer highly skilled personnel). This means that PostNL has partially said farewell to the traditional postmen and women with their substantial fixed-hour contracts, and has gone looking for new postal delivery workers willing to work more flexible hours and at a lower rate. This is a complex process in content-related terms, certainly when it concerns large numbers of employees and considerable social consequences.

To realize benefits in personnel transformation, a proper consolidation of benefits management is a critical success factor. The targets with regard to workforce increase and reduction are connected to “owners” who are individually responsible for achieving the targets and the consequent benefits. By also embedding the desired changes in the plans and estimates, management is guaranteed to focus on achieving benefits. A special project office monitors the desired increases and reductions. In real-life practice, it turns out that the assumptions that were made in the original plan must be adaptable. For example, if the reduction in postal employees is slower than specified in the plan, the recruitment of new employees will come under pressure. Economic developments also have a strong influence on the employee turnover. Therefore, this requires continual re-appraisal of the workforce. A complicating factor is the fact that this appraisal should occur not only at the national but also at each regional level.

Conclusion

In this article we have examined the way in which benefits management can contribute to transformations. The most important contribution is that it creates clarity about what and who is involved in the transformation, and how it is to be implemented. This is accomplished by working out which activities contribute to achieving the strategic aims, how benefits are realized, and who is responsible for realizing the benefits. With this, benefits management strengthens the foundation for successful transformations. It ensures that success factors are in place, such as ensuring clear goals, delivering a concrete strategic plan, and outlining clear roles and responsibilities. This leads to deeper insight into the transformation on the part of stakeholders, so that if adjustments have to be made as a result of changing circumstances, a better result is guaranteed.

A good plan is half the work. That is why this article pays so much attention to the elaboration of the benefits realization diagram and the approach to benefits management. In formulating the plan, it is essential to have a clear idea of the way in which benefits must be realized and how they contribute to achieving strategic objectives. It is at least as important to attune the approach to the organization and the nature of the transformation that is to be implemented. With a transformation that is directed toward cost-saving, you will have to measure and achieve results differently than if the goal were a change toward a more customer-oriented and innovative organization.

After the planning phase, the next major challenge during the entire transformation is to keep the focus on managing the benefits achieved, including those realized by the line organization. This is a process of change in itself. And by managing the process in a structured way, as the leader of the transformation, you introduce a mindset geared to realizing benefits. You keep all eyes focused on the benefits, so that people are more oriented to achieving the business benefits offered by change.

References

[Blen10] M.W. Blenko, M.C. Mankins and P. Rogers, The Decision-Driven Organization, Harvard Business Review, June 2010, p. 54-62.

[HBR10] Harvard Business Review, How hierarchy can hurt strategy execution, Harvard Business Review, July/August 2010, p. 74-5.

[Hest09] M. van Hest, E. Keyzer, L. Kox and P. Becker, Kostenoptimalisatie, De kaasschaaf biedt geen duurzaam soelaas, in: Excellent Presteren, KPMG, 2009.

[Hunt09] R. Hunter and G. Westerman, The Real Business of IT: How CIOs Create and Communicate Value, Harvard Business Press, October 2009.

[Kell11] S. Keller and C. Price, Beyond Performance: How Great Organizations Build Ultimate Competitive Advantage, Wiley, June 2011.

[Mank05] M.C. Mankins and R. Steele, Turning Great Strategy into Great Performance, Harvard Business Review, July/August 2005.

[Mart10] R.L. Martin, The Execution Trap, Harvard Business Review, July/August 2010, p. 64-71.

[McKi06] McKinsey, Organizing for successful change management: A McKinsey Global Survey, June 2006.

[McKi10] McKinsey, McKinsey Global Survey results: What successful transformations share, 2010.

[Mile10] R.H. Miles, Accelerating Corporate Transformation, Harvard Business Review, January/February 2010, p. 68-75.

[Neil08] G.L. Neilson, K.L. Martin and E. Powers, The secrets to Successful Strategy Execution, Harvard Business Review, June 2008.

[OGC03] OGC _Office of Government Commerce, Managing Succesful Programmes, second edition, TSO: London, 2003.

[Post11] PostNL, Business Strategy, www.postnl.com, 2011.

[Skin04] D. Skinner, Primary and secondary barriers to the evaluation of change, Evaluation 10/2, 2004, p. 135-154.

[Ward06] J. Ward and E. Daniel, Benefits management: Delivering value from IS & IT investments, John Wiley & Sons Ltd., 2006.