Due to mind-blowing technological developments in the automotive industry and changes in customer behaviour, mobility in 2030 will be dramatically different. The autonomous driving car enables highly optimised transportation and asset utilisation. Autonomous driving depends on decision making without human intervention, which is made possible by algorithms and Artificial Intelligence (AI). These algorithms and AI enable direct and automated access to mobility platforms for logistic planning and real time interaction with objects and vehicles. As a result, new business models will arise and fulfil new and sometimes untapped customer needs. The how we move is more and more facilitated by algorithms, based on our previous or expected behavior, external triggers and/or events. The actual working of these algorithms should not be a black box and therefore assurance on algorithms will be an item of interest in the coming years.

Introduction

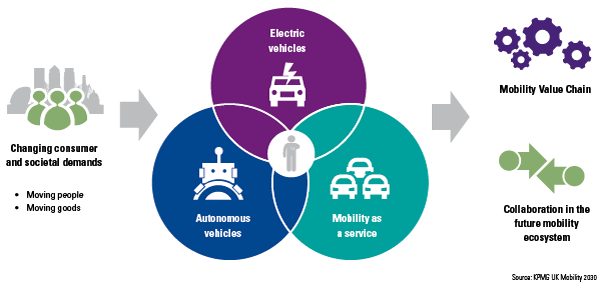

The automotive industry is at the forefront of a radical digital transformation. The introduction of digital technologies impacts the industry in many different ways. Three forces will fundamentally transform how we move people and goods in the future, as can be seen in Figure 1 below.

- Firstly, electrification: basically all conventional power sources will be replaced by electric powertrain technologies that will enable sustainable transport with zero emissions. Battery capacity will rapidly become more affordable and various alternatives for the conventional lithium-ion batteries are being introduced.

- Secondly, the rise of ‘mobility-as-a-solution‘ services that includes the mind shift from ‘ownership’ to ‘usage’ of the car. Platform-based business models are optimising underutilisation amongst car owners, connecting the various forms of transport and offering a one-stop-shopping concept.

- Thirdly, and most importantly, is the technological breakthrough of autonomous driving cars. Currently, many new car models are being introduced with these new driving features. Initially, incorporated into Advanced Driver Assistance Systems that provide ‘autopilot’ functionalities, but eventually with an increasing level of autonomy.

Figure 1. Overview of mobility ecosystem changes ([KPMGUK17]).

The future mobility ecosystem is very different

The mobility ecosystem will look very different in the future, but why? The current ‘one-car-one user’ is very inefficient and costly as most of the time a car is not used. The total fleet of passenger cars in the Netherlands consists of approximately 8,3 million vehicles ([BOVA17]). Most of them (approximately 95% according to [Morr16] sit idle each day and are parked. People spend a lot of their time in traffic jams ([ANWB17]). The increasing urbanisation will increase the time spent in traffic. In addition, the current TCO (Total Cost of Ownership) for cars is an important component of the total household budget. In summary, the current one-car-one-user model results in underutilised assets. Therefore, the current model makes the car an expensive form of transportation.

The autonomous vehicle (AV) might be the main reason that the ownership model will shift from one-car-one-user to one-car-multiple-users. These new user communities do not care who owns the car, but see the transportation from A to B as a service. Therefore, the current car ownership model will evolve to a ‘mobility-as-a-service’ model. Mobility subscriptions to car share schemes provide consumers with more convenience, clear costs and fixed rates and kilometre packages. In addition, it solves looking for a parking place in front of your house in a fully congested city! As a driving licence might no longer be needed for these new vehicles, the number of potential users is almost unlimited. New user groups are being tapped. People who were not able to use a car for transportation, now have the opportunity to use autonomous cars as a passenger as they do not need to be able to drive the car itself. Therefore, the growth of travelled kilometres per person will primarily take place in the 0-30 years old segment and the 50 and older segment ([KPMGUK17]). The AV will provide more independence for these segments. However, as these new solutions require high volumes of users and a large infrastructure (assets, technology, connectivity and data analytics), a consolidation of mobility service providers is likely. Service aggregators are a single point of contact for consumers that provide the solution to integrate the required components for autonomous driving. In summary, the autonomous car will enable:

- lower costs per kilometre (no driver costs, new energy sources, benefits from economies of scale and longer vehicle lifetime);

- more efficiently used vehicles (up to five times the number of kilometres compared to human operated cars);

- tapping new markets with potential users who previously did not own a car, or were not able to use a car for transportation;

- major ecosystems to consolidate (therefore reduce in number) and the type of ecosystem player will change as new industries are entering the market.

Autonomous driving will reinvent the value chain, new platform based business models will be introduced

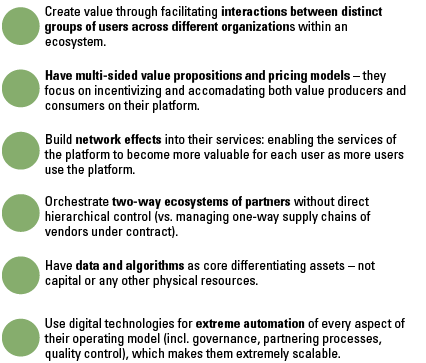

Next to a transportation object, the autonomous car is also more and more a platform that enables extra digital revenues, which will become a very important source of income for the automotive industry. In the Global Automotive Executive Survey of 2017 [KPMG17], 85 percent of the nearly thousand car executives from 42 countries surveyed were convinced that their company will realize a higher turnover through a digital ecosystem (up to ten times). In this ecosystem, payments might become a very important new activity to enable automated interactions between cars and objects, for example to pay for charging the battery at a public charging point. To be successful, companies in the mobility industry will change. Platform organisations are the ones that will actually change the automotive industry. These organisations are mainly driven by data and algorithms. As can be seen in Figure 2 below, the rules of the game for platform business models are significantly different.

Figure 2. How to be successful with platform business models ([KPMGNL17-1], [Alst16], [Chou15], [Evan16], [Tiwa13]).

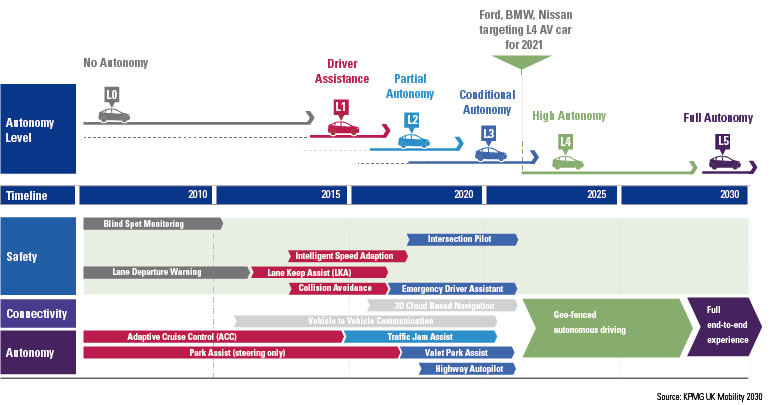

The autonomous driving car is coming, developments are accelerating

Although we are still talking in the future tense, the technology is already available. Start-ups, for instance, increasingly compete to mass-produce next-gen radar and LiDAR systems (3D road images) to enable autonomous driving. Original Equipment Manufacturers (OEM) are introducing these new technologies in their products, as can be seen in Figure 3 below. Many services have been launched and/or are gradually becoming available. Some of the ‘flagship events’ we have listed, indicate a continuous and accelerating introduction of developments with respect to autonomous driving. The autonomous driving car is increasingly becoming mature, and the industry is very active. In short, in 2017:

- Ford acquired dynamic-shuttle firm Chariot (a mobility integrator);

- General Motors acquired Sidecar (sharing a ride as a new transportation service);

- Volkswagen invested in cab-hailing start-up Gett (on demand mobility as counterpart to taxi app Uber);

- Europcar acquired car-sharing start-up Bluemove (car sharing and hourly rental service);

- GM bought Cruise Automation (autonomous driving tech firm);

- Ford acquired Pivotal, a data analytics company to gain valuable customer insights;

- Waymo, the former Google self-driving car project in 2009, is ready for the next phase: their driverless transport services will soon be introduced to the public;

- Audi introduced their first production car (the new A8) with level-3 autonomous driving functionality in September 2017.

Figure 3. KPMG UK Mobility 2030 Scenario Analysis – Stretch Case ([KPMGUK17]).

Fully accelerating, or do we anticipate short circuits and power outages?

As depicted above, technology developments are accelerating, and car manufacturers design new computers and algorithms at an increasing pace. But are we pushing this, or do we really understand what customers really value? Do we have the right skill set to integrate/aggregate other ecosystem elements? If all technology is readily available, what is limiting the speed of developments?

- change of regulations (approval from European and national level to drive autonomously);

- new insurance models (shift of accountability from driver to car);

- privacy regulations (possibly limit the transfer of data and usage of data by platforms to offer personalised services);

- service integrators and providers that take full responsibility for the whole value chain;

- the roll out of 5G mobile connection technology (specifically the required short latency times) that enables communication between vehicles;

- smart infrastructure with digital traffic beacons and road signs (to avoid misinterpretations of the algorithms);

- local area networks standard (cross brand communication);

- customer adaption.

The autonomous car must be a ‘good robot’

In autonomous cars, the importance of algorithms and the way of checking these ‘digital brains’ should not be underestimated. As often the possibilities are endless, but do we still understand the choices that are made by technology?

We have seen an increasing number of applications where humans depend on algorithms. The autonomous car has to make ethical decisions, based on algorithms that have been developed by IT specialists. How do we know the car makes the right decision?

As we already explained in our report The connected car is here to stay [KPMGNL17-2], these topics will be increasingly important for safeguarding consumer trust. An example is the working of a navigation system. To guide the driver from A to B, it is essential that the system meets the following conditions:

- the quality of the data needs to be good;

- the algorithm, basically the instructions given, must be correct;

- the route advice should serve the interests of the driver; it should be an independent advice of course, it should not be the case that the algorithm has a preference for a route along a particular brand of fuel stations or shopping centres.

Conclusion

Autonomous driving is reinventing the value chain and new platform based business models will be increasingly introduced. Next to a transportation object, the autonomous car is also more and more a platform that enables extra digital revenues, which will become a very important source of income for the automotive industry. However, the importance of the algorithms and the way of checking these ‘digital brains’ should not be underestimated.

Although accountants primarily evaluate financial statements and annual reports, the accountancy sector can certainly play a key role in this game. Assurance by accountants has been a proven method in business to provide confidence and trust to users. Accountants have the capabilities to provide ‘assurance of systems’ about the accuracy of the processes and algorithms. This requires a considerable investment in a rapidly changing market. However, public trust in this modern digital society should be handled with care, as this trust could very well be the bottleneck for a quick adoption of the autonomous driving vehicle. Might this public trust be key for a fast, digital transformation to the new mobility ecosystem?

The Netherlands is ready for the autonomous vehicle

The Dutch ecosystem for the autonomous vehicle is ready. The intensively used Dutch roads are very well developed and maintained. Many different large road construction projects have been finished during recent years ([RIJK17-1]). Other indicators, like the telecom infrastructure, are also very strong, as can be seen in the yearly OpenSignal top 10 for 4G coverage footprint [OPSI17], in which the Netherlands holds a high position.

In addition, the Dutch Ministry of Infrastructure has opened the public roads to large-scale tests with self-driving passenger cars and lorries. Since 2015, the Dutch rules and regulations have been amended to allow large-scale road tests ([RTL17], [TNO17]).

In collaboration with the federal road authority (Rijkswaterstaat), and the ministry of Infrastructure, the federal vehicle authority (RDW) has the option of issuing an exemption for self-driving vehicles ([RIJK17-2]). Companies that wish to test self-driving vehicles must first demonstrate that the tests will be conducted in a safe manner. To that end, they need to submit an application for admission.

Public/private partnership do further accelerate the development of automotive expertise and innovation capacity. Strong examples are the Automotive High Tech Campus in the Eindhoven area and the connected TU Eindhoven university ([TUEI17]), which has a specific Smart Mobility faculty. Start-ups such as Amber Mobility ([TECR17]) are challenging existing parties and are broadening existing beliefs and behaviours.

References

[Alst16] M.W. Alstyne, S.P. Choudary, G.G. Parker, Platform Revolution: How Networked Markets Are Transforming the Economy and How to Make Them Work for You, W.W. Norton & Co., 2016.

[ANWB17] ANWB, Filegroei zet door in 2016, ANWB.nl, https://www.anwb.nl/verkeer/nieuws/nederland/2016/december/filezwaarte-december-2016, 2017.

[BOVA17] BOVAG, Mobiliteit in cijfers, BOVAGrai.info, http://bovagrai.info/auto/2016/bezit/1-2-ontwikkeling-van-het-personenautopark-en-het-personenautobezit/, 2017.

[Chou15] S.P. Choudary, Platform Scale: How an emerging business model helps start-ups build large empires with minimum investment, Platform Thinking Labs, 2015.

[Evan16] R.S. Evans, R. Schmalensee, Matchmakers: The New Economics of Multisided Platforms, Harvard Business Review Press, 2016.

[KPMG17] KPMG, Global Automotive Executive Survey, KPMG, 2017.

[KPMGNL17-1] KPMG NL, Platform Advisory – Talkbook, Amstelveen: KPMG Advisory N.V., 2017.

[KPMGNL17-2] KPMG NL, The Connected Car is here to stay, Amstelveen: KPMG Advisory N.V., 2017.

[KPMGUK17] KPMG UK, Mobility 2030, KPMG UK, 2017.

[Morr16] D.Z. Morris, Today’s cars are parked 95% of the time, Fortune.com, http://fortune.com/2016/03/13/cars-parked-95-percent-of-time/, 2016.

[OPSI17] OpenSignal, State of Mobile Networks: Netherlands (September 2017), Opensignal.com, https://opensignal.com/reports/2017/09/netherlands/state-of-the-mobile-network, 2017.

[RIJK17-1] Rijksoverheid, Infrastructure PPP projects, Government.nl, https://www.government.nl/topics/public-private-partnership-ppp-in-central-government/ppp-infrastructure-projects, 2017.

[RIJK17-2] Rijksoverheid, The Netherlands as a proving ground for mobility, Government.nl, https://www.government.nl/topics/mobility-public-transport-and-road-safety/truck-platooning/the-netherlands-as-a-proving-ground/, 2017.

[RTL17] RTL Nederland, Brabant laat zelfrijdende auto’s testen op de openbare weg, RTL Nieuws, https://www.rtlnieuws.nl/geld-en-werk/brabant-laat-zelfrijdende-autos-testen-op-de-openbare-weg, 2017.

[TECR17] TechCrunch, Amber Mobility to launch self-driving service in the Netherlands by 2018, TechCrunch.com, https://techcrunch.com/2017/04/25/amber-mobility-to-launch-self-driving-service-in-the-netherlands-by-2018/, 2017.

[Tiwa13] A. Tiwana, Platform Ecosystems, Elsevier Science & Technology, 2013.

[TNO17] TNO, Truck platoon matching paves the way for greener freight transport, TNO.nl, https://www.tno.nl/en/focus-areas/urbanisation/mobility-logistics/reliable-mobility/truck-platoon-matching-paves-the-way-for-greener-freight-transport/, 2017.

[TUEI17] TU Eindhoven, Strategic Area Smart Mobility, TU Eindhoven University of Technology, https://www.tue.nl/en/research/strategic-area-smart-mobility/, 2017.