The introduction of IT in organizations was rather turbulent. Under the motto “First there was nothing, then the bicycle came”, everyone had to learn to deal with the effects of IT on people and processes. This article describes the development of IT and the role of auditors related to the investigation into the quality of the internal control on behalf of the financial audit. IT-related laws and regulations are discussed as well as KPMG’s involvement with professional organizations and university study programs.

For the Dutch version of this article, see: Automatisering en IT-audit

The beginning of IT

Since 1965, computers were introduced in organizations, mostly for simple administrative applications. In this period the accountancy profession had a slight wake-up call when during control work at audit clients (assistant) auditors desperately mentioned: “They bought a computer.” At that time, there was no IT organization yet whatsoever.

Start automation with batch processing

Simple processes were automated and processed by computers (that meanwhile had been introduced by IBM, BULL, and UNIVAC) that could only perform one process at a time. The responsibility for automation lay almost always with the administrative function of the organization.

The required programs were written in programming languages such as assembler or COBOL. The elaboration of the required functionality occurred on pre-printed forms after which the programmers themselves had to record the instructions on punch cards. These large quantities of punch cards were read in the computer center and recorded on magnet tapes, after which processing took place. The output was printed on paper. The same process was used for the processing of mostly administrative data. The computer was controlled through the so-called Job Control Language (JCL). Computer operators could initiate operations with the aid of these JCL processes.

In time, complexity grew and the expert in the area of computer control programs – the systems programmer – entered the scene. Both the quality and effectiveness of the internal control measures within organizations were pressured as this new function of system programming could manipulate the results of processing out of sight of the internal organization.

The accountancy profession quickly acknowledged that automation could be of influence on the quality of the system of internal control measures within organizations. Already in 1970, the Netherlands Institute of Register Accountants (NIVRA1), issues Publication number 1 with as its title Influence of the administrative automation on the internal control. That same year the Canadian Institute of Chartered Accountants issues the book Computer Control Guidelines, followed in 1974 by Computer Audit Guidelines. In 1975, the NIvRA Publication 13 follows: The influence of automated data processing on the audit.

Use of the computer in the audit

It was a local step for an auditor to quickly choose to use the client’s computer or an in-house computer to provide the client with the required information on behalf of the audit. Standard packages such as AudiTape were marketed. Within KPMG, a department was created in 1971 entitled Automation & Control Group with programmers that ensures that the audit control practice was fully equipped. Next to the much-used statistical “currency ranking” sampling method, a better method is developed, called the sieve method.

Needless to say, it was stressed that there is a need for the audit client to attend the processing of the software developed by auditors or standard audit software used.

The development of the COMBI tool (Cobol Oriented Missing Branch Indicator) within KPMG offers the possibility using test cases to acknowledge the “untouched branches” in a program, which can be applied efficiently during the development phase of programs.

Foundation of KPMG EDP Auditors

After a short start-up phase of a few years, in which specialized accountants used audit software on computers at audit clients, the Automation & Control (AC) group was established in the period 1971-1973. This group consisted of financial auditors with IT affinity (which were trained and rotated every three years) and programmers for the development of queries and audit software, such as the abovementioned COMBI.

In 1974, it was decided to establish a separate organizational unit entitled KPMG EDP Auditors (KEA, hereinafter KPMG). The attention of the auditor moved to engaging (IT Audit) experts, who had to establish whether the embedded system of measures of internal control in the organization was also anchored in the configuration of the information system. This also happened with respect to acquiring certainty that application programs developed by/under responsibility of the user organization would be processed unchanged and in continuity.

Specialized knowledge of the auditor’s organization was required due to the complexity arising from the introduction of large computer systems with online/real-time facilities, database management systems and standard access control software (COTS, Commercial-Off-The-Shelf). After all, the organization must be able to identify the impact that this new technology will have on internal controls and be able to recognize the implications for the auditor’s work.

It is in that context that in 1974 it was decided to issue a professional journal entitled Compact (COMPuter and ACcounTant). Initially, it was primarily intended to inform the (financial) audit practice, but was increasingly highly appreciated by other organizations, mainly audit clients.

Introduction of complex computer systems

Since 1974, the application and usage of computers accelerated as the new computers could perform multiple tasks simultaneously. In addition, an infrastructure was created that allowed the user organization to collect data directly. The IT organization therefore became an independent organizational unit and was usually positioned within the Finance hierarchy.

IBM introduced the operating system MVS (Multiple Virtual Systems) and shortly after (1975) software under the collective name of Data Base Management Systems (DBMS) was marketed. The emphasis of IT applications was placed on on-line/real-time functionality. Other computer suppliers introduced similar systems.

The efforts of auditors aimed at assessing the quality aspects of automation initially focused mainly on assessing the measures of physical security of the computer center and the availability of a tested emergency plan.

When the development of batch environment to online/real-time environment continued, the importance of logical security, as well as quality of procedures, directives and measures in the automation organization came to the fore. Think of the arrangement of access control; back-up, and recovery procedures; test, acceptance and transfer procedures of application software; library management, etc.

The introduction of complex computer systems not only meant a migration from classically organized data to a new IT environment, but also a migration of control measures to higher software layers (access control systems, sub schemes within DBMS’s). The entire data conversion project from the classical IT environment to on-line/real-time necessitated a sound planning of the conversion, define phases, set-up procedures for data cleansing, determining completeness and correctness of data collection and security measures during the entire project.

Many Compact issues have discussed this complexity of the above-mentioned profound events and the impact on the internal and financial audits.

Minicomputer systems

More or less simultaneous with the introduction of large complex mainframe computer systems, smaller computer systems were introduced. As these became bigger, they were called mid-range computers.

For the KPMG organization this meant further specialization, as the introduction of minicomputer systems in SME organizations usually had different consequences for the design of the system of internal controls and for the security measures to be taken in these organizations.

KPMG authors successively published articles in Compact with subjects such as the reliability of administrative data processing with minicomputers; the decentral use of small computers: a new problem, and also: the influence of the implementation of small-scale automation on the audit.

Newer versions of mid-range computer systems have a more complex architecture which enables better possibilities for realizing a securely operating IT organization. Especially the security options for the popular IBM AS/400 system were extensively published.

In addition, the security of PC systems and end-user computing was addressed. A Compact Special was entirely devoted to the manageability and security due to the increasing use of PC networks (including risks, methods, audit programs and tooling).

Auditing of information systems

Atypical of automation is that for data processing, the development of hardware and supporting software occurs (almost) simultaneously. Since the beginning of the seventies, auditor, and more specifically the experts specialized in IT auditing, also focused on audit information systems to verify whether internal control measures were not only correctly configured in application programs, but also in the underlying operating system software.

A research methodology entitled “System Assessment approach & financial audit” was developed early on in The Netherlands and periodically updated further to frequent usage. Later – in 1998 – this methodology was followed up by the internationally adopted Business Process Analysis (BPA) method.

The rapid increase of electronic payments and the mapping of its consequences for the manageability as a result of these new developments should be mentioned as well as the discussions about the use of encryption and possible consequences of legislation.

The quality of the system development organization was also investigated. This development ultimately led to Enterprise Resource Planning (ERP) systems as a further integration of applications occurred, and subsequently, to improve the control of ERP Projects, Quality Assurance measures were introduced. In literature, both underexposed management aspects were discussed at ERP implementations and the complexity of defining and implementing approvals.

E-business advances rapidly too. Electronic payments on the Internet become more or less self-evident, e-mail conventions were developed. Assessing the critical infrastructural security mechanisms, such as Public Key Infrastructure (PKI), to which end a national framework of audit standards and procedure needed to be developed, became important to IT Auditors. The KPMG PKI standards framework was later adopted internationally in the WebTrust standard. Above all, KPMG focused on the assessment of risk management and E-business environments.

Information Security Policy

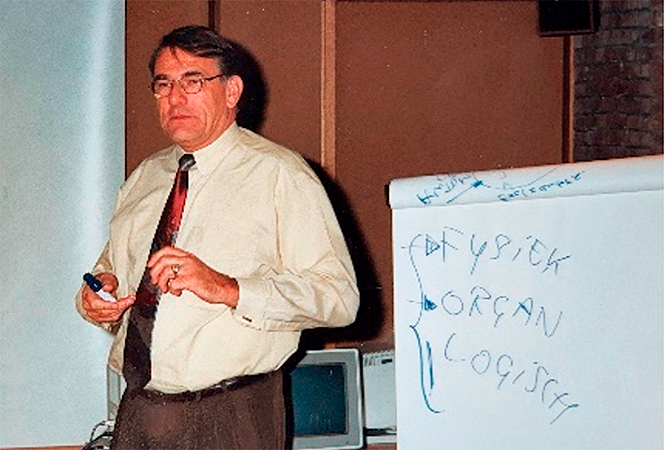

Information Security has been in the spotlight ever since the start of the automation of data processing. Since the early eighties, the subjects of organizational security, logical security, and physical security (see Figure 1), as well as back-up, restart and recovery and fallback options were considered in conjunction.

Figure 1. Class about Information Security (Dries Neisingh at the University of Groningen). [Click on the image for a larger image]

In the 90s, the Information Security policy was highlighted as a sound foundation for information protection. Since then, many KPMG authors have shared their knowledge and experience of Information Security in almost all Compact volumes.

Artificial Intelligence and Knowledge Based Systems

At the beginning of the eighties, an investigation was started within KPMG examining the possibilities of the use of Artificial Intelligence (AI) in the audit. In 1985 “Knowledge-Based Systems (KBS): a step forward into the controllability of administrative processes” was introduced as a result of, amongst others, the developments in AI, higher processing speeds and larger memories. The KBS software does not contain human-readable knowledge but merely algorithms that can perform (in the rule-base) processes based upon externally stored knowledge.

In the following years, there were new developments, as evidenced by publications on Structured Knowledge Engineering (SKE), developed by Bolesian Systems. Further to the above, KPMG published about “Control software and numerical analysis” and about “Testing as a control technique”.

Microcomputer in the audit

After the successful growth of the use of computers in the (financial) audit, the attention partly spread to the use of the microcomputer in the audit. In 1983, an automated planning system became operational. Subsequently, a self-developed audit package was demonstrated with which file researches could be executed.

The use of the micro in organizations to support administrative information processing was extensively published, as well as its use at the auditor as a control tool. The micro was therefore used both as stand-alone and as part of a network.

Within KPMG, two projects were being started, notably the development of software for connecting the computer of the audit client with the auditor’s micro and the development of control programs for processing on the auditor’s micro. KPMG’s Software Engineering department researches software engineering, operating systems (e.g. UNIX), computer viruses, electronic payment, and the debit card.

IT outsourcing

Organizational scale and/or financial capacity sometimes mean that automated data processing was being outsourced to computer/IT service organizations that usually make use of available standard packages on the market. Especially IT outsourcing grew rapidly in the nineties and early this century.

Jointly founded IT organizations – as a shared service center – arise as well. An example is the founding of six computer centers spread across the country on behalf of healthcare insurers administrations. Each health care insurer uses the same functionality and was on-line/real-time connected to one of the regional computer centers. From the start of this special cooperation, KPMG was involved as IT Auditor for overall quality assurance. Several opinions were issued on the quality aspects of the newly established IT organization, as well as the effective operation in continuity of these organizations and on the automated business rules and controls of the software. After all, the health insurance funds themselves carried out the user controls.

NBA publication 26 entitled Communications by the auditor related to the reliability and continuity of automated data processing, paid attention to these problems. Later, Publication 53 was published regarding Quality opinions on information services. In practice these were named Third Party Statements (TPMs).

IT-related laws and regulations

Inspection and certification of IT

Since the beginning of the 80s, the subject of IT inspections and certifications regularly popped up on the agenda. The foundation “Institute to Promote Inspection and Certification in the Information Technology”2 was established. The Netherlands Standardization Institute (NNI3) was already working on a standard for the quality system for software. Within KPMG, much attention was paid to the possibility of issuing opinions on software quality systems, but also for the certifying of software and development systems. Compact, for instance, published widely on the issues at hand.

Finally, the foundation KPMG Certification was established. In January 1998, it officially received the charter “Accreditation of BS 7799 Certification”4, because by the end of 1997, ICS (International Card Services, now part of ABN AMRO Bank) had received the first Dutch certificate for this international Information Security standard.

In November 2002, the above accreditation of KPMG Certification was followed by the first accreditation and certification of PinkRoccade Megaplex (now part of telecommunications company KPN) for the TTP.nl certification scheme “Framework for certification of Certification Authorities against ETSI TS 101456”. This refers to the servicing of digital certificates for making use of digital IDs and signatures. Today, this is comparable to the eIDAS certification.

Memorandum DNB

The Memorandum “Reliability and continuity of automated data processing in banking” published by the Dutch Central Bank (DNB) in 1988 was in itself no revelation. Since the start of KPMG’s IT Audit department, specialized IT Auditors were deployed in the audit practice of financial institutions, related to the assessment of internal controls in and around critical application software, and measures taken in the IT organization.

Various Compact issues show that the IT Audit involvement was profound and varied. My oration at the University of Groningen in 1991 entitled “There are banks and banks” critically contemplates this Memorandum.

It is worth noting that in April 2001, the DNB presented the Regulation Organization and Control (ROB), in which previous memoranda such as the one regarding outsourcing of automated data processing were incorporated.

Computer crime

Since the mid 70s, publications under the heading “Computer Abuse” increasingly appear. Several “abuse types” were subsequently described in Compact. The subject remains current.

In November 1985, the Minister for Justice installs the Commission “Information technology and Criminal Law” under the presidency of Prof. H. Franken. KPMG was assigned by this commission to set up and perform a national survey among business and government to acquire insight (anonymously) in the quality and adequacy of internal controls and of security controls in IT organizations.

In the report that appears in 1987, the image sketched about the quality and effectiveness of the measures taken was far from reassuring, both in small and in large IT environments. The committee’s conclusion was therefore (all things considered) to make criminalization of computer-related crime applicable, taking into account the findings presented, if there were “breaches in secured work”.

Privacy

The creation of laws and regulations regarding privacy (as the protection of personal data) has a long history. At the end of 1979, the public domain was informed in a symposium called “Information and automation”, which focused on the imminent national and international legislation regarding data protection, privacy protection and international information transport.

Subsequently, Compact was being used as an effective medium for employees and especially clients and relations to inform them on developments. In cooperation with the then Data Protection Authority5 a “New brochure on privacy protection” was issued by KPMG further to the Data Protection Act (Wpr) being enacted in 1988. Especially since 1991 there were many publications on privacy authored by KPMG employees. KPMG also conducted the first formal privacy audit in the Netherlands together with this privacy regulator.

In 2001, the new Dutch Data Protection Act (Wbp) replaced the Wpr – due to the EU Data Protection Directive 95/46/EC. At that time, an updated Privacy Audit Framework was also introduced by a partnership of the privacy regulator with representatives from some public and private IT auditing practices, including KPMG.

An interview published in Compact 2002/4 with the chairman of the Board entitled “Auditor as logical performer of Privacy audits. Personal Data Protection Board drives Certification”.

Transborder data flow

Already in 1984, an investigation was performed into the nature and scope of data traffic crossing borders and especially into the problems and legislations in several countries.

In 1987, KPMG and the Free University of Brussels published the book entitled Transborder flow of personal data; a survey of some legal restrictions on the free flow of data across national borders. The document consisted of an extensive description per country of the relevant national legislation, from Australia to Switzerland and the OECD Guideline. It discussed the legal protection of personal data, the need for privacy principles and the impact of national and international data protection laws on private organizations.

Encryption

The use of encryption rapidly increased partly because of the introduction of (international) payment systems. Other applications of encryption also took place, such as external storage of data devices. In 1984, the Ministry of Justice considered initiating a licensing system for the use of encryption in case of data communication. The granting of such licenses should also be applied in the case of the use of PCs, whether or not included in a network.

Partly further to the outcome of KPMG’s investigation “Business Impact Assessment cryptography” and pressure from the business community, any form of encryption regulation was refrained from.

Legal services

Expanding KPMG product portfolio with legal IT services was a logical consequence of above developments, which occurred since 1990 with the recruitment of lawyers with IT and Information specialization. The regulatory developments not only referred to the above-mentioned legal subjects, but also to the assessment and advise of contracts for the purchase of hardware, software packages and to the purchase of software development as well as escrow (source code depository), dispute resolution, with probative values of computer materials and copyright, etc.

The Compact Special 1990/4 was already entirely devoted to the legal aspects of automation. In 1993, due to the developments in IT and law, KPMG published a book entitled 20 on Information Technology and law. KPMG authors and leading external authors contributed articles. In 1998, one of the KPMG IT lawyers obtained her doctorate with her PhD thesis Rightfully a TTP! An investigation into legal models for a Trusted Third Party. The legal issues had and still have many faces and remain an important part of servicing clients.

IT Audit and Financial Audit

The relationship between the IT Audit and the Financial Audit practice has been strengthened over the years. As organizations started using IT more intensively in (all) business processes the meaning of anchoring the internal control and security measures in the IT environment became inevitable. Determining that the system of internal controls in organizations was anchored in continuity in the IT environment required employing IT Audit expertise. Initially, the IT Audit was supporting the audit; however, the influence and meaning of the use of IT in organizations became so immense that seemingly solely employees with both a RE and RA qualification would be capable to perform such an audit.

The publication of the Compact article 2001/3 entitled “Undivided responsibility RA for discussion: IT-auditor (finally) recognized” dropped a bombshell within the accountancy profession. Many KPMG authors published leading articles on the problem. The subject had already been considered in 1977 with the publication of the article “Management, Electronic information processing and EIV – auditor”. “Auditor – Continuity – Automation and risk analysis” is extensively covered in 1981. From 1983 onwards, articles on audit and ICT (Information and Communication Technology) were published quite regularly.

In recent years, Compact has explored this decades-long relationship between IT auditing and financial auditing in several articles, such as in Compact Special 2019/4 “Digital Auditing & Beyond”. In this Compact issue, the article by Peter van Toledo and Herman van Gils addresses this decades-long relationship.

The broadened field of IT Audit(or)

Over the years, it became clear that the quality on the general internal, security, and continuity controls significantly affected the possibility to control the IT organization and with it the entire organization and its financial audit. Subsequently, the effectiveness and efficiency of the general IT controls system attracted in-dept attention.

From the 80s onwards, KPMG’s Board decided to broaden the service offering by also employing (system) programmers next to auditors with IT expertise, as well as administrative information experts, computer engineers and the like. And finally, even (IT) lawyers. Consequently, a wide range of services arose. The KPMG organization’s pioneering role within the industry also served as a model for the creation of the professional body NOREA.

As the integration of ICT continued to take shape, a further expansion of knowledge and services in that direction took place. Some employees obtained their PhD (i.c. promotion to dr.) or an additional legal degree (L.LM), and some even became (associate) professor.

The Chartered Accountants associated with KPMG all were a member of the NIVRA, now the NBA. The activities employed in this organization on behalf of the audit practice were mentioned before. It took quite some time before, in addition to NIVRA, the professional association of EDP Auditors would be established (1992). The admission requirement of membership of the Netherlands Order of Chartered EDP Auditors (NOREA) was to have completed a two- or three-year EDP Audit study at one of the three universities that offered this new degree. Of course there were transitional arrangements for those who had proven knowledge, expertise, and experience. Like NiVRA, a Board of Discipline was installed at NOREA.

Within NiVRA there was much interest in the development of IT and its consequences for the financial audit. However, the expertise as far as IT was concerned, was initially mostly concentrated in the Netherlands Society for Computer Science of IT professionals (NGI6), in which KPMG played an important role in various working groups such as “Policy and risk analysis”, “Physical security and fall-back”, “Security supported by application software”, “architecture”, “Privacy protection and EDP Audit”.

University studies

A prominent practice like KPMG has a mission to also provide a stimulus to research and education in the field. Therefore, KPMG has made an important contribution over the years to university education in the area of both EDP Auditing and on the influence of the use of ICT on the control of organizations and on the financial audit.

It meant the development of an EDP Audit study program and on the other hand the setting up of new university chairs / professorships in the area of IT Audit and administrative organizations.

- Already in 1977, Dick Steeman was appointed at the Erasmus University Rotterdam. Steeman took office as extraordinary professor with pronouncing the public lesson “Management, Electronic information processing and EIV-auditor”.

- In 1990, Dries Neisingh was appointed professor at the University of Groningen, department Accountancy, chair “reliability aspects automated information systems”. The speech’s subject was “the Memorandum regarding reliability and continuity of automated data processing in banking (Memorandum DNB): there are banks and banks”.

- At the beginning of 1991, the appointments of professor EDP Auditing at the Erasmus Universiteit of Cor Kocks and Hansen Moonen at the Tilburg University followed.

- In 1994, professor Ronald Paans joined KPMG. He already was a professor EDP Auditing at the VU Amsterdam (Free University).

- In 2002, dr. Edo Roos Lindgreen was appointed professor “IT in Auditing” at the University of Amsterdam. In 2017 he was appointed professor “Data Science in Auditing”.

- In 2004, dr. Rob Fijneman became professor IT Auditing at Tilburg University.

Figure 2 shows the management of KPMG’s IT Audit practice in 1987 with some of the above-mentioned people.

Figure 2. Management of KPMG’s IT Audit practice upon retirement of Han Urbanus (in 1986). From left to right Dick Steeman, Dries Neisingh, Hans Moonen, Tony Leach, Han Urbanus and his wife, Jaap Hekkelman (chairman of NGI Security), Cor Kocks and Herman Roos. Han Urbanus and Dick Steeman jointly founded KPMG EDP Auditors and started Compact magazine. [Click on the image for a larger image]

Compact

The introduction of Compact in April 1974 was an important initiative of KPMG’s IT Audit Board. The intention was to publish an internal publication on IT subjects on a regular basis. The standard layout became primarily one or a few technical publications, IT developments, ABC News (Automation, Security, and Control), new books and articles included in the library and finally “readers comments”. In the first years, ABC News articles were frequently drawn from EDPACS7 magazine and other international publications.

The first issue started with the article “the organization of testing” and a contemplative article about “software for the benefit of the financial audit: an evaluation”. In the second issue, the first article was continued with subjects such as test monitoring, acceptance tests and system implementation.

Over the years, Compact becomes increasingly widespread: both clients and potential clients appear highly satisfied with the quality of the articles and the variety of subjects. Compact developed into a professional technical magazine! The authors were KPMG employees with occasionally contributions of external authors.

Since 1983, articles regularly addressed the relationship between Audit and IT. In Compact Specials, the editorial staff renders the meaning of such a special issue: “as usual every year a Special appears on audit and IT Audit. In the meantime, it has become habitual to confront CPAs and Register EDP Auditors (RAs, REs and RE RAs) with the often-necessary deployment of EDP Auditors in the financial audit practice after the completion of the audit of the financial statements and after the cleaning of files and prior to the layout of files for the new year”.

On the occasion of 12.5 years of Compact on Automation & Control, the book 24 about EDP Auditing was published in 1986. The book contained a bundle of updated articles from Compact, written by 24 authors. The preface started with a quote by Benjamin Disraeli: “the best way to become familiar with a subject is to write a book about it”.

Increasingly, Compact Special issues were published. In 1989, a Special appeared on “Security” and in 1990 on “The meaning of EDP Auditing for the Financial auditor”. Five external authors from the business also contributed to this Special also as well as a public prosecutor and Prof. mr. H. Franken.

In the run up to the 21st century, it became rapidly clear for many organizations and more especially for the IT sector as well as for EDP Auditors, that problems would definitely arise at the processing of data by application software as a result of the millennium change. Compact became an important medium to attract attention to this both internally and externally. Compact 2000/1 looks back with the article “Across the threshold of the year 2000, beyond the millennium problem?”.

The anniversary issue 25 years of Compact appeared in 1999/2000. Of the 57 authors 50 were employed by KPMG in various functions as well as seven external authors (among them a few former employees). It was a dashing exploit: a publication of 336 pages with 44 articles. The introductory article was called “From automation and control to IT Audit”. In the article “essential assurance over IT” largely goes through the clusters of articles.

Barely recovered from the millennium problem, the introduction of the euro presented itself. In Compact 2000/1 attention was paid to the introduction of the euro entitled “and now (again) it is time for the euro”. The Compact issues 2000/5 and 2000/6 were entirely devoted to all aspects of the conversion to the euro. Articles were being published under the header: “Euro conversion: a sound preparation is not stopping at half measures” and “Implement the euro step by step: drawing up a roadmap for the transition”. And: “Validating the euro conversion”, “Euro emergency scenarios” and “Review of euro projects”.

Conclusion

In the thirty years that were briefly reflected in this article, a lot has happened in the area of the development and application of IT in business and government. For (financial) auditors, it was not easy to operate in this rapidly changing environment. Training courses were not available, and knowledge was sparsely present within or outside the organization.

KPMG has taken the lead to making problems accessible for accountants by the creation of KPMG EDP Auditors and the simultaneous start of publishing Compact magazine. In addition to that, next to auditors, different types of IT professionals were also recruited. Many are to be thanked (the promoters and the successive generations) for the fact that with the start of KPMG EDP Auditors and the broadening of knowledge areas, the emerging market demand could be served adequately. KPMG has timely facilitated that sufficient time and investments could be leveraged for education and product development; this is why KPMG EDP Auditors could lead the way in the market.

The thirty years (1971-2002) have flown by. A period in which many have contributed and can look back with satisfaction. This is especially true for the author of this article who has summarized an earlier article of almost sixty pages.

Notes

- Currently, the Royal Netherlands Institute of Chartered Accountants (NBA).

- Original name: “Stichting Instituut ter bevordering van de keuring en Certificatie in de Informatie Technologie (ICIT)”.

- Currently the Netherlands Standardization Institute is named NEN: NEtherlands Norm.

- Currently known as ISO 27001 accreditation.

- The Data Protection Authority as had different names, aligned to the prevailing Privacy Act. Currently it is named Authority Personal Data (in Dutch: “Autoriteit Persoonsgegevens”), before that the Personal Data Protection Board (in Dutch: “College Bescherming Persoonsgegevens”) and initially the Registration Office (in Dutch: “Registratiekamer”).

- Currently the KNVI, the Royal Netherlands Society of Information Professionals

- EDPACS was issued by the EDPAA (EDP Audit Association); currently, the ISACA Journal is published by ISACA, the International Security Audit Controls Association.