Europe’s largest fintech event, Money20/20, was held in Amsterdam this year (4 to 6 June 2018), accentuating the positive development of the Dutch fintech climate. With an estimated number of 430 companies currently active in the Dutch fintech market – which includes over 100 companies that were added last year ([HOLF18]) – it is clear that fintechs are on the rise in the Netherlands. How did Dutch fintech evolve in the past ten years?

Introduction

Fintechs combine financial services with innovative technologies and cover more than just payment and banking services. Both fintech (innovative technology in financial services) and fintechs (companies using innovative technology as basis for their financial service offering) can be found in a broad array of domains, such as insurance (InsurTech), regulations (RegTech) and pensions (PensionTech). Regardless of the type of fintech, a vast amount of fintechs, both in the Netherlands and abroad, focus on radically improving specific parts of the traditional financial services models (such as the universal banking model) through innovative technology – thereby ‘unbundling’ traditional models.

However, fintech is not the exclusive domain of new entrants, but is also increasingly embraced by existing players in the market and can also take on hybrid forms, such as corporate spin-offs or partnerships. In the Netherlands, we have seen both new entrants (such as Adyen, Binck and DeGiro) and existing players’ spin-offs (such as MoneYou, Peaks, Payconiq) entering the Dutch fintech sector in recent years.

Figure 1. Fintech growth, see also [KPMG17]. [Click on the image for a larger image]

The past ten years of fintech in the Netherlands at a glance

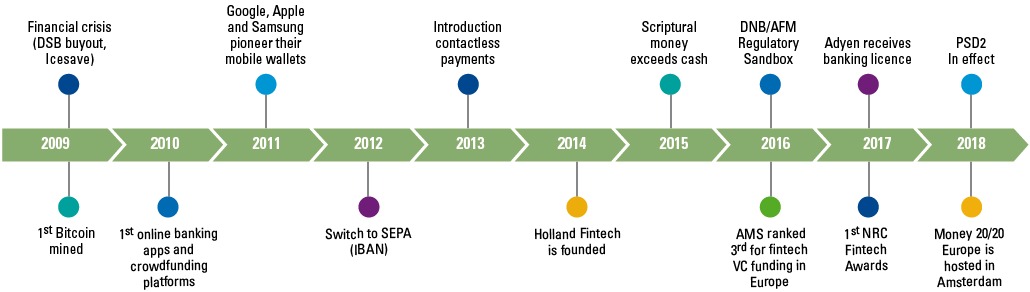

Alerted by the 2007-2012 financial crisis, regulators turned up the heat on the major players in the financial services industry, such as the Dutch universal banks and more controversial players, like IceSave and DSB. The combination of increased regulatory pressure, increased aversion against the conventional financial sector, exponential technological developments and changing customer demands, enabled new and existing fintechs to increasingly gain traction in the years to come.

Since then, the Dutch fintech market evolved quickly. The steep growth of the Dutch fintech landscape was earmarked by, among other things, the establishment of Holland Fintech in 2014, a fintech hub aimed at empowering people and organizations to improve their economic circumstances by making use of financial innovation. It was also during this period that ‘fintech’ became better known to a larger public (or merely the buzzword?), nicely illustrated by the increasing number of search queries on Google [GOOG18].1

Dutch fintechs

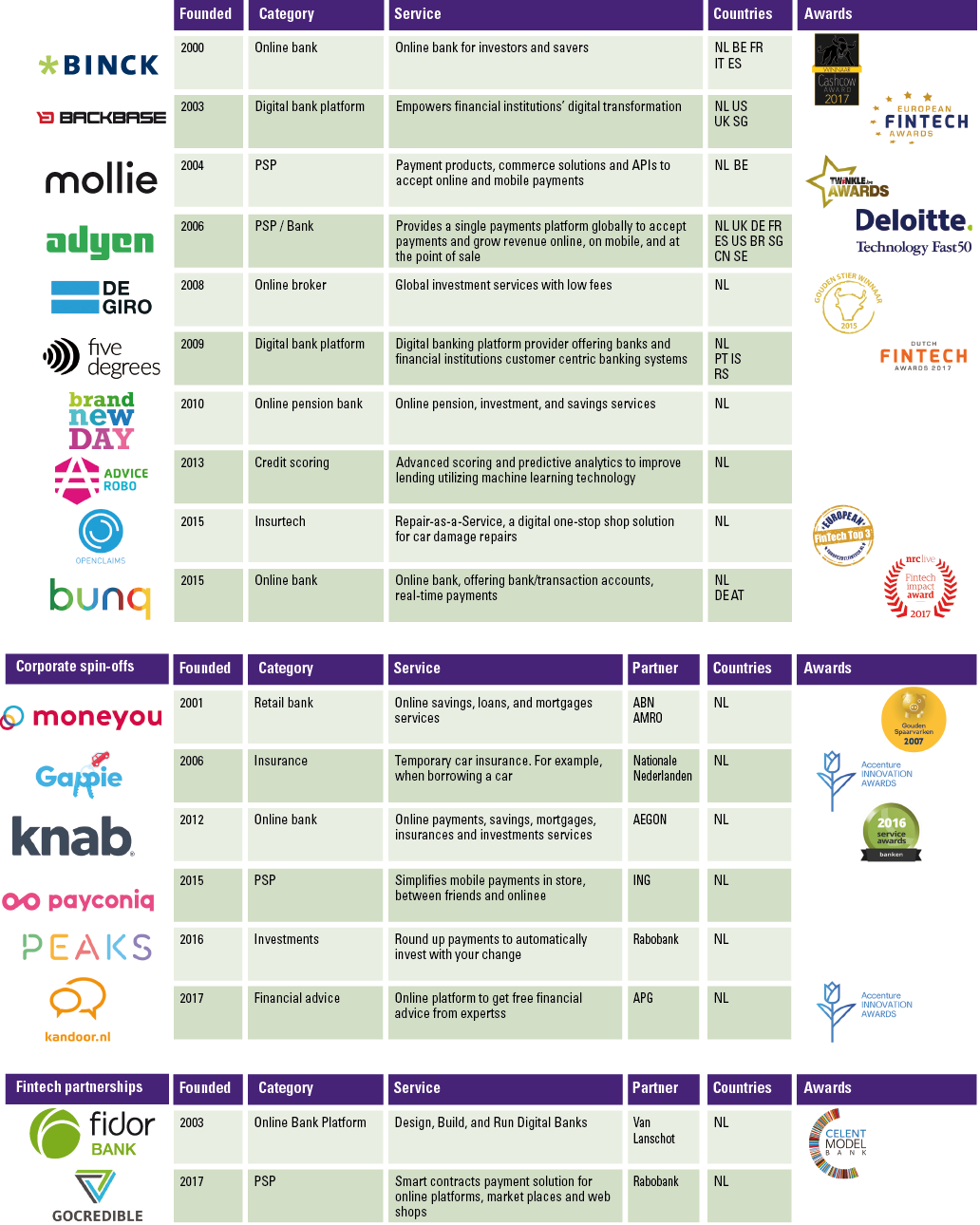

A well-known example of a Dutch fintech is Bunq, which evolved into a Dutch mobile bank after obtaining a banking license in 2015. Another example is the ‘unicorn’ by the name of Adyen; the Amsterdam-based payments service provider, and one of the largest fintechs in Europe. Adyen was founded in 2006, has grown exponentially in the past years to over EUR 1 billion of revenues in 2017 and recently obtained a banking license. Finally, DeGiro, a Dutch brokerage company founded in 2008 by former Binck Bank employees, offering brokerage services to retail investors is another example. All three have in common that they grew organically and exponentially, on their own, from start-up to scale-up and beyond.

Fintech and the establishment

Diversification in the Dutch financial services sector increases as new entrants enter the market and become part of the financial services value chain. While developments such as PSD2 may accelerate the introduction of new players, history shows that a period of consolidation usually follows after a period of diversification, leaving the best to survive. Developments like PSD2 may give new entrants a ‘free ride’, while incumbents need to open their doors and allow access to transaction-data to such third parties – running the risk of just becoming infrastructure providers.

Nevertheless, existing players (i.e. large banks and insurers) have not rested on their laurels. The largest banks of the Netherlands – ING, ABN AMRO and Rabobank – started numerous initiatives to reap the benefits of fintech. Examples are: ABN AMRO’s further digitalized subsidiary MoneYou, an online platform for mortgages, loans and savings; the ‘ING Ventures’ fund, used by ING to invest in promising fintechs around the world; and corporate spin-offs like Rabobank’s Peaks, a new initiative to automatically invest your spare change. Other examples of spin-offs are Gappie (Nationale-Nederlanden), providing insurance when borrowing a car from friends, and Kandoor (APG), providing free of charge online financial advice. In its very origin even Knab should be mentioned, a bank founded in 2012 as a spin-off of the insurer Aegon.

Established Dutch financial services organizations also benefit from fintechs through partnerships. Van Lanschot, for instance, has a cooperation with the German provider of digital banking solutions Fidor.

Although this overview is not even nearly complete, these examples are illustrative for the broader developments within the Dutch fintech landscape.

The Dutch regulatory landscape

The innovative business and operating models brought along by fintechs, also required a different regulatory view, as innovation typically does not fit neatly into existing laws and regulations. Also, many new players face difficulties complying to the stringent regulatory regimes in financial services.

In 2016, the AFM and DNB therefore launched a new approach, the ‘regulatory sandbox’, aimed at providing bespoke regulatory solutions and easing market access, to offer more room for innovation in the financial sector. Both regulators also assess existing policies, rules and regulations on whether they require changes to further accommodate new developments ([DNB18]). In addition, DNB and AFM jointly launched the ‘InnovationHub’, to which (new) market players can address their regulatory questions; another measure to further accommodate innovation.

Opportunities arising from regulatory developments in the European market, such as PSD2 and Open Banking, further stimulate the rise of fintech in Europe as well as in the Netherlands.

Investment climate and location

The Dutch culture, tech-savvy citizens, the well-developed financial sector and the constantly growing tech sector, are forces to be reckoned with. Amsterdam alone estimates a number of 15,000 people employed in Amsterdam’s fintech sector ([IAMS18]). Also, the Dutch mobile-banking penetration, talent development and (digital) infrastructure offer a flourishing breeding ground for fintech.

What’s next?

The global fintech ecosystem continued to mature at an accelerated pace over the course of 2017. In 2018 and onwards, we expect numerous big trends to impact the direction in which fintech is developing. Continued innovation in artificial intelligence (AI) and blockchain as an underlying technology, the introduction of Instant Payments and Open Banking and the rise of online (lending) platforms (similar to other tech platforms like Booking.com and JustEat) are among these trends. Also, the rise of new challenger banks and participation of the big techs in the financial services domain are among the trends influencing the next years’ fintech ecosystem – globally as well as in the Netherlands.

Table 1. Our top 10 predictions for 2018 ([KPMG18]). [Click on the image for a larger image]

Examples of Dutch fintechs

Table 2. Examples of Dutch fintechs. [Click on the image for a larger image]

A decade of Dutch fintech

Figure 2. A decade of Dutch fintechs. [Click on the image for a larger image]

Notes

- Google trends: ‘fintech’ searched for 23 times in 2013, 71 times in 2014, 333 times in 2015, 862 times in 2016, 974 times in 2017 in the Netherlands.

References

[DNB16] De Nederlandsche Bank (DNB) & The Dutch Authority for the Financial Markets (AFM), Meer ruimte voor innovatie in de financiële sector, DNB.nl, https://www.dnb.nl/binaries/Meer-ruimte-voor-innovatie-in-de-financi%C3%ABle-sector_tcm46-361363.pdf?2017080320, 2016.

[GOOG18] Google Trends, Fintech, Google, https://trends.google.nl/trends/explore?date=all&geo=NL&q=FinTech, 2018.

[HOLF18] Holland Fintech, Dutch fintech Infographic 4.0, Hollandfintech.com, https://hollandfintech.com/2018/01/growing-number-fintech-companies-netherlands/, 2018.

[IAMS18] I Amsterdam, Fintech industry in Amsterdam, IAmsterdam.com, https://www.iamsterdam.com/business/key-sectors/financial-and-fintech/fintech, 2018.

[KPMG17] KPMG, The Pulse of Fintech Q4 2017, Global analysis of investment in fintech, KPMG International, https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2018/02/pulse_of_fintech_q4_2017.pdf, 2017.

[KPMG18] KPMG, Fintech predictions 2018, KPMG International, https://home.kpmg.com/xx/en/home/insights/2018/02/fintech-predictions-2018-fs.html, 2018.